Market View - 2nd Quarter 2026

“I have said many times and cannot say it too often that the experience of years as a stock operator has convinced me that no man can consistently and continuously beat the stock market though he may make money in individual stocks on certain occasions. No matter how experienced a trader is, the possibility of his making losing plays is always present because speculation cannot be made 100% safe. Wall Street professionals know that acting on inside tips will break a man more quickly than famine, pestilence, crop failures political readjustments or what can be called normal accidents. There is no asphalt boulevard to success on Wall Street or anywhere else” – Concluding observations of Jesse Livermore, arguably the most successful investor in Wall Street history as recalled in Edwin Lefevre’s book, “Reminiscences of a Stock Operator”.

Last Quarter Review

Global equity markets continued to grow steadily until the 28th February, before falling sharply following the decision of the United States to attack Iran after the negotiation attempts to persuade Ayatollah Ali Khamenei and the Iranian regime to abandon its nuclear weapons programme had failed. What many had hoped would prove to be a short-lived war continues and threatens to engulf the whole region following retaliatory attacks by Iran on other Arab states where US bases are located including Bahrain and the UAE.

Iran’s attacks on several ships travelling through the Strait of Hormuz (which accounts for around 20% of global oil traffic) and the failure of the US and its allies to ensure safe passage has resulted in the price of West Texan Intermediate (WTI) oil rising from around $65 a barrel just before the war to more than $100 by quarter end. This in turn resulted in equity and bond markets markets falling dramatically as the threat of sustained higher energy prices may result in global recession, with investors fearing the US Federal Reserve Bank (Fed) may abandon further interest rate cuts.

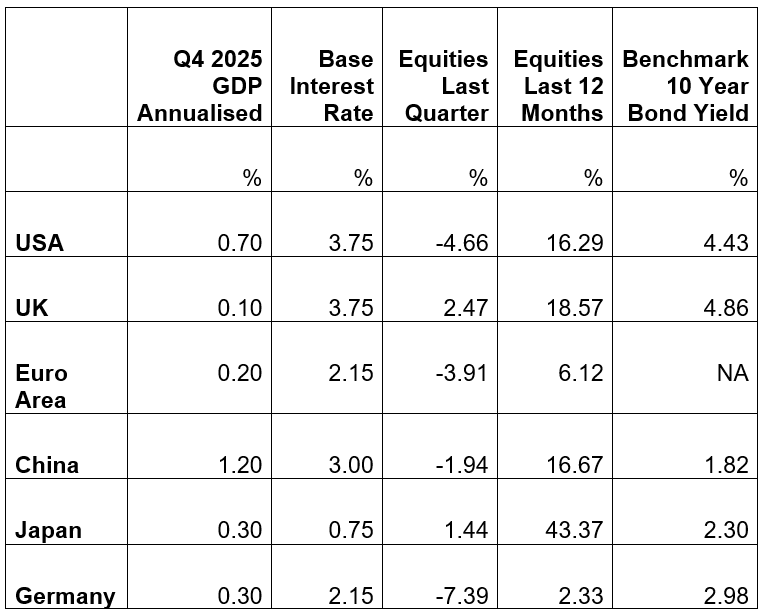

At its March meeting of the Federal Open Markets Committee (FOMC), the Fed left its federal funds rate unchanged at 3.5% – 3.75% for a second consecutive month noting that whilst economic activity has been expanding at a solid pace, job gains remain low while inflation is higher than they would wish. It noted that while the implications of the Iranian war are uncertain it still expects to make one interest rate reduction in 2026 and another in 2027.

The Fed revised upwards its GDP growth forecast for 2026 to 2.4% (from 2.3%), and 2027 to 2.3% (2.0%), while unemployment expectations remain unchanged for 2026 at 4.4% and slightly higher for 2027 at 4.3% (4.2%). Both personal consumption expenditures (PCE) and core inflation are now expected to be higher this year at 2.7% (2.4% & 2.5%).

Bond markets appear concerned about potential inflation following the commencement of the Middle East war as the yield on the benchmark 10-year US Treasury Note rose from 3.97% on the 27th February to 4.43% at end March, the highest since July 2025. Global equity markets also declined with the S&P 500 falling to 6582 from its all-time high of 6979 at the beginning of the year and 6946 just before the attack on Tehran.

The US dollar has as risen following the conflict as investors have sought safe havens and is currently trading at more than100 when measured against the DXY, a basket of other currencies weighted on market size. Gold on the other hand which had prior to the conflict risen to almost $5500 fell below $4400 before closing the quarter at around $4700 but remains up more than 50% over 12 months.

In the UK, the Bank of England (BoE) unanimously voted to keep the Bank Rate at 3.75% in March 2026, as the conflict in the Middle East has caused a sharp rise in global energy and commodity prices, pushing up household fuel and utility costs and raising business expenses. Prior to this shock, domestic prices and wages had been showing continued disinflation.

Higher energy prices are expected to push the consumer price index (CPI) to between 3% and 3.5% over the next few quarters, though a slowdown in economic activity from rising costs could limit second-round effects. The UK’s benchmark 10-year gilt yield surged above 5%, the highest since July 2008, before settling quarter end at 4.86%, as higher energy prices prompts a sharp shift in Bank of England expectations from the two anticipated cuts to two or three hikes in 2026.

Prior to the start of the Iran war, the FTSE 100 (made up primarily of globally focused companies with international earnings) had risen 9.86% from 9931 at the beginning of 2026 to 10910 on the 27th February, before losing most of these gains by the end of the quarter and closing at 10176. In currency markets, sterling remained strong against the dollar at $1.32, little changed over the quarter.

In the Eurozone, the European Central Bank (ECB) kept its key interest rates unchanged at its March meeting, with the deposit facility at 2.00%, and the main refinancing rate at 2.15%. In light of the anticipated impact of higher energy prices due to the conflict, the ECB has revised down growth projections in 2026 from 1.2% to 0.9% and from 1.4% to 1.3% in 2027, with 2028 unchanged at 1.4%, while inflation is expected to average 2.6% (previous 1.9%) in 2026, 2.0% (1.8%) in 2027 and 2.1% (2%) in 2028.

The People’s Bank of China (PBOC) kept key lending rates at record lows for a tenth consecutive month in March, in line with market expectations, with the one-year Loan Prime Rate (LPR), the benchmark for most corporate and household borrowing at 3.0%, while the five-year LPR, which anchors mortgage rates, held at 3.5%. The cautious stance reflects surging oil prices and Middle East tensions clouding the inflation outlook, alongside Beijing’s lower 2026 growth target of 4.5%–5%, its weakest since 1991, reducing the urgency for broad easing.

The Bank of Japan (BoJ) left its key short-term rate unchanged at 0.75% at its March 2026 meeting, keeping borrowing costs at their highest since September 1995. Policymakers believe Japan’s economy is recovering moderately but warned that escalating Middle East tensions cloud the outlook, and that they will continue raising rates and adjusting monetary support if growth and inflation unfold as projected, noting real rates remain significantly low.

The Vix index which is a measure of market volatility and risk closed at a new 2026 high in the last week of March having almost doubled from its end 2025 level. High yield spreads in the bond market exceeded 4% over their equivalent US Treasury interest rates with the Oracle Credit Default Swap (CDS) exceeding its 2008 highs during the subprime crisis.

GDP Data shown are to the 31st of December 2025; Interest Rate, Equity & Sovereign Benchmark Bond Yield Data are to the 31st of March 2026; Equity Indices used: US – S&P 500, UK – FTSE 100, Eurozone – Euro Stoxx 50, China – Shanghai Shenzhen CSI 300, Japan – Nikkei 225, Germany – Xetra Dax; Benchmark Sovereign Bond Yield Data courtesy of Trading Economics.

Current Considerations

Investors who had hoped that the war between the United States and Iran would be over quickly following the attack on Tehran on the 28th February under the dual objective of eliminating their nuclear threat and facilitating regime change are slowly realising this could be another long-drawn conflict. Investors are busy re-evaluating the potential impact on the US and global economy as the average price of gas hit $4 per gallon in America on the 31st March for the first time since 2022.

West Texas Intermediate (WTI) oil futures refined in the US also hit $100 in March for the first time since 2022 while the CBOE Volatility Index known as Wall Street’s fear gauge rose 50% in March and has more than doubled since the 1st January. The price of gold and silver meanwhile collapsed following the outbreak of the war, while the yield on the benchmark 10-year US Note initially fell as investors sought safe havens but has since risen again reflecting the bond market’s inflationary concerns about prolonged hostilities.

Prior to the last trading day of March, all three major US Wall Street indices had been set to record their worst month and quarter since 2022. However, US stocks surged on the 31st March after Iranian President Pezeshkian was reported as saying he was open to ending the war with the US, Israel, and GCC members under conditions.

The S&P 500 and the Nasdaq 100 gained nearly 3%, while the Dow jumped 1,000 points. The development reflected Washington’s attempts to de-escalate the conflict following the suspension of attacks by President Trump, aiming to restore flows of tankers through the Strait of Hormuz and halt the surge in energy prices.

Additionally, comments from Fed Chair Jerome Powell speaking at Harvard University on the 31st March, stating he saw the inflation outlook as stable and the central bank would not need to raise interest rates to counter oil price increases, helped ensure a strong Wall Street rally on the last day of the quarter. Comments from other influential Fed governors like Stephen Miran suggesting interest rates should continue to be reduced despite the increased energy prices, helped restore calm and confidence on Wall Street.

As we begin the second quarter, the news feeds from the Middle East conflict remain volatile and unpredictable. One day the headlines suggest a peace deal is imminent only for Iran to subsequently supposedly deny any negotiation, while the USA threatens to obliterate the oil production on Kharg Island (which is responsible for 90% of Iran’s supply) or worse.

However, history teaches us that no matter what global events occur there is no substitute for a risk adjusted investment portfolio made up primarily of global equities (with a high allocation to Wall Street stocks) and investment grade fixed income (with a high allocation to US Treasuries). Historically over the long term, a portfolio heavily weighted towards these two asset classes on a risk adjusted basis has outperformed all other combinations.

In the past decade, some speculators have made money from investing in bitcoin and other crypto currencies. However, over the past 12 months the value of Bitcoin has halved and sadly as is usual with investment manias, most private investors piled in near the top around twelve months ago and are now both out of pocket and disenchanted.

Recent revelations following the release of more Epstein Files suggests Bitcoin is an elite creation designed to make money for a select group of criminal insiders, which highlights the risks of embracing new investment ideas without advice from professional advisers who specialise in putting together risk adjusted portfolios with the primary emphasis on capital preservation. When considering the ideal combination of asset classes for investment portfolios, the primary considerations are historic long-term returns, yield, volatility, and liquidity.

It is for this reason that we have rarely considered physical gold or gold stocks as part of a risk adjusted portfolio. Admittedly an investor in gold bullion over the past 12 months would have more than doubled their money, until the bubble burst last quarter and bullion fell around 20%.

Once again anecdotal evidence suggests most private investors piled into gold earlier this year and many are now nursing losses and shocked by the rapid reverse in value of the asset class. Gold bullion also suffers from the combined disadvantages of lack of liquidity and zero yield.

Last quarter, anecdotal evidence suggests informed investors sold gold and exchanged this for US Treasuries as the threat of stagflation appeared on the horizon because of the Middle East conflict driving up energy prices, which in turn will potentially drive-up inflation. In such a scenario an asset with zero yield and low liquidity pales in comparative value to a fixed income investment in the most liquid market in the world (except for the dollar currency market) yielding more than 4%!

As Jesse Livermore famously observed, “No matter how experienced a trader is, the possibility of his making losing plays is always present because speculation cannot be made 100% safe”. History shows that the shrewd investor focuses on capital preservation, and a balanced risk adjusted portfolio.

An analysis on CNBC using Morningstar data last September analysed the returns of gold stocks, real estate and long-term government bonds over a 30-year period between October 1st1995 and September 30th, 2025. The results showed equity returns averaged 10.5% per annum, real estate 8.9% pa, gold 8%, and government debt 5%.

“Gold glitters but earnings compound,” said Pat Beaird, of Beaird Harris Wealth Management in Dallas. “Historically, our view has always been that equities have more staying power as an inflation hedge, and If I’m going to subject a portfolio to that level of volatility, I’d rather have it in the highest returning asset class.”

By adopting portfolios invested in global equities focused primarily on Wall Street stocks and in bond funds focused heavily on US Treasuries and other prime First world government bonds, investors can be sure their asset allocation combines optimal historic long-term returns, yield, volatility, and liquidity.

Forward Outlook

History shows that while unexpected wars and military conflicts such as is now occurring in the Middle East inevitably cause volatility and collapse in values across most market sectors on Wall Street in the short term, the long-term trajectory of the market is rarely impacted for long. Remember the adage, in the short term the market is a voting machine, but in the long term it is a weighing machine, i.e. value will prevail over emotion over time.

Typically, during the initial periods of new conflicts, the stock market will respond with a sharp setback as investors sell some of their equities and “flee to safety” in the form of less volatile asset classes such as US Treasuries, gold, the US dollar and even cash. History shows that the average decline immediately following a significant geopolitical event is around 5% – 6%.

Interestingly however, market data suggests that, since the Second World War, in 19 of the 20 most severe setbacks, markets had returned to pre-conflict levels within an average of just 28 days, normally bottoming around two to three weeks after the initial panic. Based on this, the adage of buy at the first sound of gunfire when others want to sell, makes more sense.

Reassuringly additional data over a long period of analysis from BNY Investments suggest that provided there is no major disruption to the global energy supply, the market’s trajectory up or down, will remain as it was pre-conflict.

Returning to fundamentals, we see no reason to change our cautiously positive views on both the US dollar (which benefits from the enormous offshore eurodollar market), and the US equity market which remains without peer in terms of the added potential of future technology gains from AI. Due to the excessive valuations attained in 2024 and 2025 however, US equities have recently begun to flatline a little while opportunities elsewhere such as the UK, Europe and Japan continue to offer superior value on a relative basis.

We would reiterate that caution is the watchword considering increasing numbers of academic analysts echoing Mike Green’s long held view that the Efficient Market Hypothesis no longer applies and that market valuations on Wall Street, and increasingly globally, reflect market flows and not fundamental rationale evaluation. For more details of this please reference last quarter’s Market View.

We remain cautiously positive on US Treasuries provided the Middle East conflict does not ultimately lead to stagflation, and cautiously confident on UK equities with particular reference to the large cap FTSE 100 stocks that comprise globally diversified businesses benefitting from US dollar exposure,

We continue to have reservations with regard to UK Fixed Interest and sterling, due to the size of the budget deficit and lack of any obvious signs of economic growth. This will become of increasing concern if the conflict in the Middle East is not resolved quickly.

When opportune, we will consider allocation to focused Bond funds with a view to taking advantage of the US Treasury yield curve un-inversion and the relative duration value that this should offer. For the present however, we maintain portfolio allocation to Fixed Interest via actively managed Bond and Multi Asset funds with a view to providing additional diversity and expertise within the sector.

Maintaining a well-diversified and balanced portfolio remains key, especially in consideration of a possible US recession in the year ahead. For now, we continue to advise a defensive portfolio allocation with an emphasis towards value and income.

As always, investment risk is at the forefront of our advice. Whilst it is often necessary to undertake adjustments in portfolio allocation to meet individual needs and preferences, we are confident that our advised portfolios will continue to remain well placed in meeting our clients’ overall objectives.

Copyright © Ash-Ridge Asset Management 1st April 2026.

Data Sources: Bank Of England; Bloomberg; Brookings Institute; Columbia Threadneedle Investments; CNBC; Economic Cycle Research Institute; European Central Bank; Financial Times; Hoisington Investment Management; Macrotrends: Macro Voices; Office for National Statistics; S&P Indices; The Economist; The Federal Reserve; The National Bureau of Economic Research; Trading Economics; UK Debt Management Office; US Debt Clock.org; US Department of The Treasury; Wall Street Journal; Yahoo Finance.

Our testimonials

I first met Anthony Kynaston some 13 years ago, when I sought advice regarding an inheritance from my late parents. He immediately impressed me with his friendly, calm, clear and professional manner, ascertaining my individual needs. Tony has since then continued to advise, plan and manage my financial affairs. This includes advice on my Buy to Let property and pension needs. He and his colleagues are always available to assist with any queries I may have. As a result, I can relax and now enjoy my retirement, leaving the complexities of financial management in their safe hands.

Ash-Ridge has provided myself and my family with friendly, professional financial advice for many years. I find them trustworthy and reliable, and would not hesitate to recommend them.

I have been working with Tony and Andrew at Ash-Ridge to manage my financial affairs for several turbulent years since 2007. They have supported me with a variety of significant decisions and administration relating to pensions and investments while dealing with ever-changing circumstances as I moved into retirement. I am very happy to work with them, and to recommend their services.

Ash-Ridge have been managing my personal pension investment portfolio for two years. I can say that I am absolutely delighted with the professional way they have handled my assets offering solid and independent advice which has been prudent and reliable. Dealing with an experienced team with first class communication and speed of response when advice is required. They are a pleasure to deal with.

Sophie and I just wanted to thank you again for all your help in remortgaging. As ever, the service was superb and efficient, we will of course be coming back!

We have been using Jane at Ash-Ridge for the last 10 years, which literally speaks volumes for the service we receive. Jane’s honest and straightforward approach is a key part in ensuring we get the deal that is best for us. She is swift and always keeps us updated throughout the entire process whilst allowing us sufficient time to make a final decision. Jane is a first class mortgage adviser and I would recommend her to anyone seeking mortgage or financial advice.