Market View - 4th Quarter 2025

“The Federal Reserve cut the federal funds rate by 25 bps (basis points or 0.25%) in September 2025, bringing it to the 4.00%–4.25% range, in line with expectations. It is the first reduction in borrowing costs since December 2024. The Fed expects to lower rates by another 50 bps by the end of 2025, and 25 bps in 2026, slightly more than expected in June.”– Source: Trading Economics

LAST QUARTER REVIEW

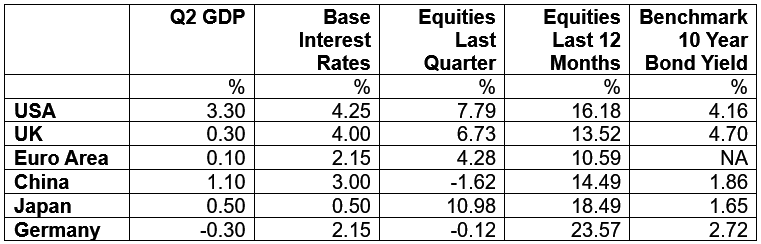

Global equity markets enjoyed strong growth as US tech stocks that have either developed Artificial Intelligence models or are using one or more of those models to power growth in their own sectors all doing well, and the major Wall Street indices of the S&P 500, Dow Jones 30 and Nasdaq 100 recording successive all-time highs during the quarter. However, these impressive returns were overshadowed by the gains made by the US domestic smaller stocks that comprise the Russell 2000 which grew by more than 12% on the back of higher demand as ordinarily cheaper overseas competitors lost market share due to the Trump Tariffs.

At its September meeting of the Federal Open Markets Committee (FOMC), the Fed revised upwards its GDP growth forecast for the next three years with 2025 now expected at 1.6% (1.4% expectation previously) 2026 to 1.8% (from 1.6%), and 2027 at 1.9% (from 1.8%). The forecast unemployment rate continues at 4.5% for 2025 but was revised lower to 4.4% from 4.5% for 2026, while for inflation, the Fed sees the PCE (Personal Consumption Expenditures) rate at 3.1% for 2025 but a little higher for 2026 at 2.6%, than the 2.4% previously forecast.

The Fed is still worried about inflationary threats with Jerome Powell emphasising in a speech on the 23rd of September that it remains elevated compared to where the central bank would like to see it, while the bond market remains relatively stable and continues to signal deflation as the bigger threat. The yield on the benchmark 10-year US Treasury Note dropped to 4.16% from the 4.24% at the end of last quarter (ELQ), while the interest rate payable on 4-week Bills dropped to 4.11% compared to 4.22% ELQ, as the yield curve continues to un-invert.

The US dollar was relatively stable when measured against the DXY, a basket of other currencies weighted on market size. During the quarter, the greenback traded within a range of $96.5 to $100.5 and ended the period broadly where it began at $97.81

In the UK, the Bank of England (BOE) reduced the Bank Base Rate by 0.25% at their August meeting, bringing it down from 4.25% to 4.0%. This was their fifth cut, and was based on evidence of easing disinflationary pressures, while at the September meeting, the BOE’s Monetary Policy Committee (MPC) voted 7–2 to leave the rate unchanged, with two members favouring a 25-bps cut to 3.75%. The MPC also voted 7–2 to slow quantitative tightening (QT) over the next 12 months from £100 billion to £70 billion which would leave it with £488 billion of bonds (mainly longer duration gilts) purchased during the period of quantitative easing (QE).

UK inflation remains above target with the CPI at 3.8% in August, although it is expected to trend back towards 2% on the expectation of subdued GDP growth, a loosening labour market, and slack in the economy. Looking ahead, the committee stressed a gradual, data-driven approach, with no pre-set path for rate cuts; thereby keeping flexibility to respond to future developments.

Despite the mixed domestic economic outlook, the FTSE 100 (which is made up primarily of globally focused companies with international earnings) rose almost 7.0% last quarter and is up 14.4% year to date (YTD), while the domestically focused FTSE 250 mid cap index rose 1.2% and is up 4.6% YTD. In currency markets, sterling remained strong against the dollar at $1.34, little changed over the period, while in the bond markets, the yield on the benchmark UK 10-year gilt was also up slightly at 4.70% (from 4.49% ELQ)

In the Eurozone, the European Central Bank (ECB) kept its three key interest rates unchanged, with the deposit facility at 2.00%, the main refinancing rate at 2.15%, and the marginal lending rate at 2.40%. ECB President Christine Lagarde said growth risks in the region are more balanced and the disinflationary process is over, with expectations for inflation broadly unchanged from June, averaging 2.1% in 2025, easing to 1.7% in 2026 before rising slightly to 1.9% in 2027.

The People’s Bank of China (PBOC) kept key lending rates at record lows for a fourth straight month in September, in line with market expectations, and followed its decision last week to leave the seven-day reverse repo rate unchanged, while the one-year Loan Prime Rate (LPR)—the benchmark for most corporate and household borrowing—remained at 3.0%, and the five-year LPR, which anchors mortgage rates, stayed at 3.5%. The decision came amid signs of easing Sino-US trade tensions, but against a backdrop of weakening domestic momentum, as industrial output in August expanded at its weakest pace since August 2024, while retail sales growth hit a nine-month low.

The Bank of Japan (BoJ) kept its benchmark short-term rate at 0.5% in September 2025, maintaining borrowing costs at their highest level since 2008 and in line with consensus, while the BoJ said it would begin selling its holdings of exchange-traded funds at about JPY 330 billion annually and real estate investment trusts at roughly JPY 5 billion, signalling further steps toward policy normalization. The central bank judged that Japan’s economy has recovered moderately as private consumption was supported by improving employment and income, though sentiment softened while exports and industrial output remained subdued, and Inflation hovered between 2.5% and 3.0%, driven mainly by food prices, especially rice, while inflation expectations edged up.

The crude oil price for West Texas Intermediate (WTI) traded in a narrow range of between $60 and $70 throughout the period and was priced around $62.5 at the end of September, compared to $65 ELQ, while Brent crude traded at $66. Gold bullion meanwhile continued its bull market run climbing from $3308 ELQ to $3858, while silver ($36.10 to $46.75) and platinum ($1348 to $1595) also rose as investors continued to look for additional safe heavens.

GDP Data shown are to the 30th of June 2025; Interest Rate, Equity & Sovereign Benchmark Bond Yield Data are to the 30th of September 2025; Equity Indices used: US – S&P 500, UK – FTSE 100, Eurozone – Euro Stoxx 50, China – Shanghai Shenzhen CSI 300, Japan – Nikkei 225, Germany – Xetra Dax; Benchmark Sovereign Bond Yield Data courtesy of Trading Economics.

CURRENT CONSIDERATIONS

As we begin the new quarter, Investors were weighing the impact of the first US federal government shutdown in nearly seven years. The last time it happened (7 years ago during the first Trump administration) it lasted 35 days.

The shutdown followed a failure by Democrats and Republicans to agree on a stopgap funding bill, with Democrats insisting that any deal should include an extension of expiring Obamacare subsidies. The impasse could furlough an estimated 750,000 federal employees, costing roughly $400 million in lost daily wages, according to the Congressional Budget Office.

The US economy which stalled in the first quarter now looks to be back on track with a strong annualised 3.3% growth in GDP achieved in the second quarter. The latest forecast from the Atlanta Fed’s GDP Now model on the 26th of September is for an annualised 3.9% GDP return for the third quarter.

The strength of the US economy has undoubtedly helped global equities recover from the trade tariff tantrum fall out seen during the first quarter. Plenty of respected market analysts and pundits had suggested back then that equities would continue falling throughout 2025 on the back of the combination of trade tariffs and exploding sovereign debt, most especially in the US, where the government borrowing of $37.5 trillion in an economy valued at $30 trillion represents 123% of GDP.

Although markets appear much happier with how the tariff negotiations have developed, there remain unintended potential consequences that could impair global economic growth in the long run. The Fed has already made it clear that they see tariffs as inflationary in the short term. As the economist Dr Lacy Hunt of Hoisington Investment Management has recently observed however, goods impacted by tariffs are likely to also see reduced demand over the longer term as a consequence of the retaliatory tit for tat tariff increases that can be expected to follow thus serving to negate the advantage the US may have had with its own tariffs initially.

Consequently, not only are tariffs likely to cause higher inflation short term, but additionally, they cause reduced capital market liquidity longer term due to an improved current account. Historically America has run a large current account deficit as imports of foreign goods have far exceeded exports.

Most US dollar proceeds from the sale of these goods to America ends up reinvested in US Treasuries or in Wall Street stocks. Hence the reason why the historic chart of the US real current account balance (which has been in deficit most years since the greenback ceased to be backed by gold bullion in 1971), is a mirror image of real net foreign investment.

As Dr Hunt observes, physical investment is made up of three types of savings, private, government and foreign and at the end of April 2025, foreign investment accounted for $17.6 trillion in US equities, $7.6 trillion in US Treasuries. $1.3 trillion in agency bonds and $4.8 trillion in corporate and other debt. The imposition of tariffs has already seen the current account deficit begin to shrink and correspondingly net foreign investment has also begun to decline and impact liquidity in capital markets.

The current American administration has imposed tariffs to try and obtain a more level playing field for domestic producers to compete with rivals from overseas whom have enjoyed many unfair advantages for decades. Dr Hunt is however concerned that unless the Fed stops worrying about transitory inflation and focuses instead on cutting interest rates to fill the liquidity void, tariffs will have a negative impact on both the US and the global economy.

From a sovereign debt perspective, the UK is in a much more precarious position. The British government has borrowed £2.68 trillion for an economy worth just over £2.7 trillion, almost 100% of GDP but without the safety net a global reserve currency, which the US enjoys. For now, both UK government debt (based on interest rates along the UK yield curve) and the sterling exchange rate suggest investors continue to view the UK as being attractive. This could quickly change, however, unless the government can clearly demonstrate fiscal responsibility and balance the books.

Maintaining investor confidence in the government bond market and sterling will prove difficult as the Bank of England continues to sell back to the market the bonds it bought with artificially created money (QE) in the period following the sub-prime banking crisis of 2008 when interest rates were low and the prices of the bonds high. These bonds are now being sold off when the reverse relationship is true, namely interest rates are much higher and the price received for selling back the bonds much lower, which according to research by several economists including those at Columbia Threadneedle Investments (CTI) is going to cost British taxpayers £134 billion or 5.4% of GDP by the time QT is finished.

Looking at the UK 30-year gilt, just prior to Covid in early 2020, the yield was around 1.25% before subsequently starting to rise sharply in 2022 following the government’s fiscal reflationary measures and is now trading at around 5.5%. It is believed that £440 billion of the total of £895 billion of the bonds purchased using QE occurred during Covid between 2020 and 2022 when interest rates were at their lowest.

The QT program began in February 2022, when the BOE ceased to reinvest maturing gilts and corporate bonds. Then in September 2022, the MPC voted to begin selling back to the market some of the £895 billion of the bonds purchased by QE, even though the prices of most these assets had fallen well below the price they had been purchased for and in many cases by more than 50%.

This accounts for CTI’s research suggesting it will cost the UK 5.4% of GDP, with an example being the purchase of the 2061 gilt in early 2020 at a price of £101, which was subsequently sold earlier this year at a price of £28, or a loss of 73%. Of course, every western central bank deployed QE in the decade following 2008 and have suffered losses to their economies through the subsequent QT process.

However, the extent of the BOE’s QE programme as a percentage of GDP far exceeded that of the Fed and other major central banks and the projected cost to British taxpayers at 5.4% of GDP is much greater than that of the USA for example where the Fed’s QT is projected to cost American taxpayers 1.4% of GDP. while the eurozone QT is expected to cost 3.0% of GDP. The decision of the BOE to slow QT down to £70 billion over the next 12 months compared to the £100 billion a year it has been selling back over the past 3 years suggests they now realise how costly their actions have been to the UK economy.

BOE governor Andrew Bailey admits the central bank’s QE programme has proved costly but suggests that the benefits were invaluable at the time and the alternative to not doing so could have resulted in an even worse economic scenario. However the unintended consequences of the BOE’s bigger (relative to GDP) QE programme meant that when QT began, long term gilt yields which had been almost identical to long term US Treasuries until September 2022, soared, albeit not helped by the additional catalyst of the Liz Truss budget (quickly reversed) as investors began to question whether the UK could be trusted with its fiscal and monetary decisions.

FORWARD OUTLOOK

For now, we see no reason to change our cautiously positive views on both the US dollar (which as the global reserve currency is insulated on the downside by the enormous offshore Eurodollar market), and the US equity market which remains without peer in terms of the potential future technology gains from the Artificial Intelligence tech sectors as well as several other related sectors that will likely benefit from these developments. The total value of publicly traded companies in the US is now at a record high of 217% of GDP, and although the price earnings ratio on the S&P 500 is very expensive by historical standards at just over 30, this is justified because it will take several years for the potential benefits from AI for the US and global economies to be fully realised.

We remain cautiously positive on US Treasuries due to the potential gains that should materialise due to the yield steepener bull market. The bond market yield curve is signalling yields will fall all the way along the duration curve but more sharply at the shorter end as the un-inversion progresses, until the whole Treasury interest rate curve has resumed its usual shape with higher yields for longer duration.

Our biggest concern for the US economy is that the Fed appears to be behind the interest rate curve, focusing too much on the short to medium term inflation risk from tariffs, when many economists suggest they should cut rates faster as the American economy is in a deflationary environment that will bring recession in 2026 if tariffs on some imports remain at current levels. Most economists and market pundits believe the base rate will eventually go to 2%, while the Fed’s projections are for 3.25% in early 2027, which may be too little and too late to avoid recession.

While we remain cautiously confident about UK equities and especially the large cap FTSE 100 stocks that comprise globally diversified businesses benefitting from US dollar exposure, we have concerns about both UK bonds and sterling for the reasons espoused above. It is worth reiterating that UK equities should also benefit from the Labour government’s Pensions Schemes Bill which is anticipated to inject over £25 billion into the UK economy, supporting crucial capital for high-growth businesses and infrastructure projects.

When opportune, we will look to increasing direct exposure to bonds with a view to taking advantage of the US Treasury yield curve un-inversion and the relative duration value that this should offer. For the present however, we will maintain allocation to Fixed Interest via actively managed Bond and Multi Asset funds with a view to providing additional diversity within this sector of the market.

Maintaining a well-diversified and balanced portfolio remains key while we consider the possibility of a US recession in 2026. For now, we continue to advise a defensive portfolio allocation with the emphasis towards value and income.

As always, investment risk is at the forefront of our advice. Whilst it is often necessary to undertake adjustments in portfolio allocation to meet individual needs and preferences, we are confident that our advised portfolios will continue to remain well placed in meeting our clients’ overall objectives.

Copyright © Ash-Ridge Asset Management 1st October 2025.

Data Sources: Art Berman: Bank Of England: Bloomberg; Brookings Institute; Columbia Threadneedle Investments; Economic Cycle Research Institute; eurodollar.UNIVERSITY; European Central Bank; Financial Times; German Federal Statistical Office; Hoisington Investment Management; Macrotrends: Macro Voices; National Bureau of Statistics China; Office for National Statistics; S&P Indices; The Cabinet Office Japan; The Economist; The Federal Reserve; The National Bureau of Economic Research; Trading Economics; UK Debt Management Office; US Debt Clock.org; Wall Street Journal.

Our testimonials

I first met Anthony Kynaston some 13 years ago, when I sought advice regarding an inheritance from my late parents. He immediately impressed me with his friendly, calm, clear and professional manner, ascertaining my individual needs. Tony has since then continued to advise, plan and manage my financial affairs. This includes advice on my Buy to Let property and pension needs. He and his colleagues are always available to assist with any queries I may have. As a result, I can relax and now enjoy my retirement, leaving the complexities of financial management in their safe hands.

Ash-Ridge has provided myself and my family with friendly, professional financial advice for many years. I find them trustworthy and reliable, and would not hesitate to recommend them.

I have been working with Tony and Andrew at Ash-Ridge to manage my financial affairs for several turbulent years since 2007. They have supported me with a variety of significant decisions and administration relating to pensions and investments while dealing with ever-changing circumstances as I moved into retirement. I am very happy to work with them, and to recommend their services.

Ash-Ridge have been managing my personal pension investment portfolio for two years. I can say that I am absolutely delighted with the professional way they have handled my assets offering solid and independent advice which has been prudent and reliable. Dealing with an experienced team with first class communication and speed of response when advice is required. They are a pleasure to deal with.

Sophie and I just wanted to thank you again for all your help in remortgaging. As ever, the service was superb and efficient, we will of course be coming back!

We have been using Jane at Ash-Ridge for the last 10 years, which literally speaks volumes for the service we receive. Jane’s honest and straightforward approach is a key part in ensuring we get the deal that is best for us. She is swift and always keeps us updated throughout the entire process whilst allowing us sufficient time to make a final decision. Jane is a first class mortgage adviser and I would recommend her to anyone seeking mortgage or financial advice.