Amid challenging conditions, there are concerns that house prices could start to fall. It may affect how much equity you own in your home and could mean some homeowners end up in negative equity.

The effects of the Covid-19 pandemic and the conflict in Ukraine mean inflation is rising in the UK and there’s a risk that the economy could fall into a recession. For many families, this may mean watching their budget more closely and people may delay plans to move or buy a home.

In turn, this can affect house prices as demand slows.

House prices increased by 9.8% in the year to March 2022

Over the last two years, house prices have experienced huge growth as demand outstripped supply. While growth is still high, data suggests that the pace is starting to slow.

According to the Office for National Statistics, house prices increased by 9.8% in March 2022 when compared to a year earlier. The average UK house price reached £278,000 – this is £24,000 higher than it was in March 2021. This compares to house price growth of 11.3% in February 2022.

Speaking to the Telegraph, property expert Paul Cheshire, a former government adviser and emeritus professor of the London School of Economics and Political Science, predicts that property prices will fall by at least 10% in the coming months.

Falling house prices can be seen as a positive for first-time buyers who are struggling to get on the property ladder. However, it can harm existing homeowners, particularly if they have a high loan-to-value (LTV) mortgage.

If you’re worried about falling property prices and the risk of negative equity, here’s what you need to know.

What is “negative equity”?

If house prices fall, there is a risk that some people will be in negative equity.

This means that the value of the property is lower than the amount that you owe on a mortgage. As a result, if you sold your home when you had negative equity, you would need to use funds from other sources to pay off the rest of the mortgage.

The current economic situation could mean that people are more likely to fall into negative equity if they have a high LTV.

The LTV ratio divides how much you’ve borrowed through a mortgage by the value of the property. So, if you’re a first-time buyer and put down a 5% deposit, your LTV would be 95%. As you make repayments or the property’s price rises, the LTV will fall.

Homeowners with a higher LTV are more likely to be affected by falling property prices as they have less existing equity in their homes. As a result, a smaller fall in prices can push them into negative equity.

While falling property prices and negative equity can be worrisome, they often won’t materially affect homeowners.

Historically, the property market has recovered following dips

If you’re worried about property prices falling, looking at how the market has recovered in the past can help.

Historically, property prices have recovered and gone on to rise further. For instance, following the 2008 financial crisis, property prices fell by more than 15% at the start of 2009 when compared to a year earlier.

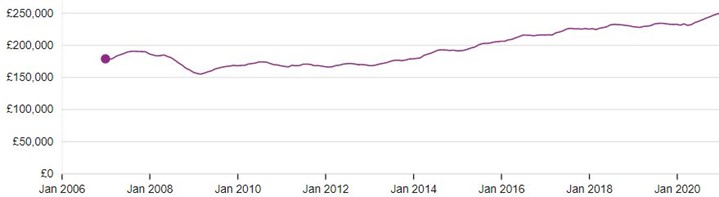

In September 2007, the average price of a home in the UK was a little more than £190,000, then fell by around £35,000 over the next two years. During this fall in house prices, many homeowners were understandably worried, but prices went on to recover and are now at an all-time high.

The graph below shows how the price of an average home in the UK has changed since 2007. While there have been several dips or periods of stagnation, the overall trend is upwards.

Source: Land Registry

It’s important to remember that while on paper the value of your property may have fallen and you’ve lost out, these losses aren’t realised unless you sell your home. So, if you don’t plan to move, falling property prices and even negative equity will have little effect on you in real terms.

If you’re selling your home during a downturn, it could affect your plans.

While you may receive an offer to sell your home for less than you’d hoped, usually the property you want to purchase will also have fallen in price. As a result, in many cases, falling property prices shouldn’t delay your plans, but you may choose to do so.

If you have negative equity, you will need to consider how you’ll pay off your mortgage and whether moving now is still the right choice for you. A delay could mean prices start to rise and your ongoing mortgage repayments will help you to get back into positive equity.

Whether you want to move home or remortgage your current property, we can help you find a mortgage that suits your needs. Please contact us to discuss your property plans with one of our team.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it.